Publication of the Aether FS Unitranche France index for the 2nd quarter 2025

Date of the event:

Paris, September 23, 2025

Publication of the Aether FS Unitranche France index for the 2nd quarter 2025

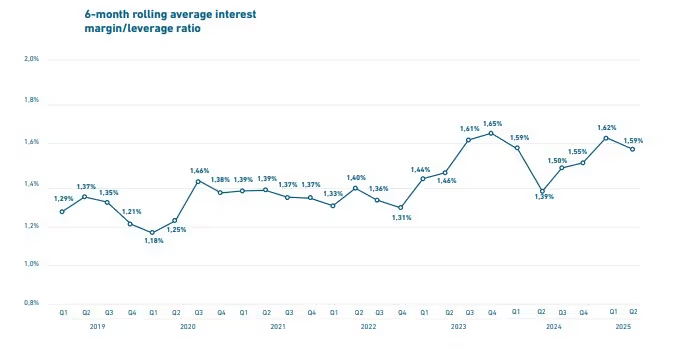

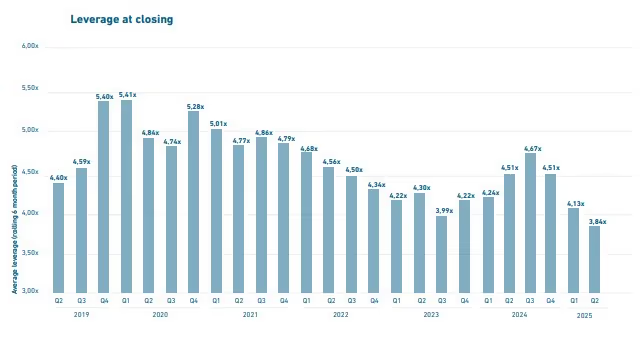

The Aether FS Unitranche France Index experienced a slight decline in Q2 2025. The margin per turn of leverage stood at 1.59%, compared to 1.62% in the first quarter. Early-year trends are confirmed, with a simultaneous decrease in spreads and leverage at closing.

6 months rolling average interest margin/levarage ratio

Evolution of Leverage at closing

Evolution of Spreads at closing

Read more articles

Publication of the Aether FS Unitranche France index for the 1st quarter 2025

Press Release

Aether FS opens new offices in Europe

Press Release

Launch of myBSPCE Value

Press Release